IGCSE Limited Company Accounts

In this lesson, we will learn the different types of capital of a limited company, how to calculate and record each of these, and the presentation in the financial statements. We will also learn how to prepare the Statement of Changes in Equity.

Key features of a Limited Company

In a limited company, shareholders’ liability for the company’s debt is limited to the amount they agreed to invest. Any legal action is taken against the company itself, not the individual shareholders.

Advantages of a limited company includes:

- Large amounts of capital can be raised

- It is easier to obtain loan than a sole trader or a partnership

- The business is managed by professionals

On the other hand, the disadvantages includes:

- Expensive and complicated procedure to start the business

- It is required to comply with more legal rules and regulations

- High administration cost

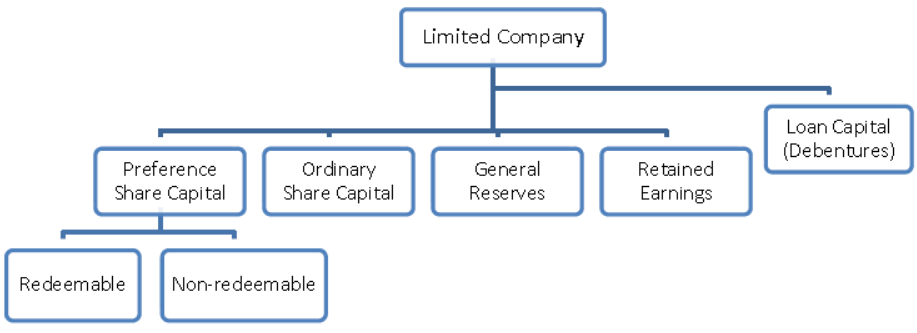

Capital Structure of a Limited Company

Ordinary Share Capital

Ordinary share capital are shares issued by a limited company to its shareholders to raise funds for the business.

Dividends paid to these shareholders fluctuate according to the company’s profit performance. As such, these shareholders have the rights to vote at the shareholders’ meetings.

However, dividends are paid only after preference share dividends are paid, and upon company’s closure, oridinary shareholders are paid after outside liabilities and preference shareholders have been paid.

The total amount of ordinary share issued to shareholders is known as Issued Share Capital.

To calculate,

Total number of shares issued × Price per share

A company may choose to call up only part of the amount payable on the shares it has issued. The amount that shareholders are required to pay is known as Called-up Capital.

To calculate,

Total number of shares issued × Price per share × Percentage of shares called

The portion of called-up capital that has been paid by shareholders is known as Paid-up Capital.

To calculate,

Total number of shares paid × Price per share × Percentage of shares called

Ordinary share dividends are not considered expenses though it is deducted from the profit for the year.

To calculate dividends,

Ordinary share capital × Rate of dividend

Alternatively,

Ordinary shares issued × Dividend per share

Preference Share Capital

Preference share capital are shares that a company issued to its shareholders where a fixed rate of dividend is payable.

Unlike ordinary shareholders, these shareholders do not have voting rights at shareholders’ meeting. However, they receive dividends before ordinary shareholders and are repaid (after outside liabilities are paid) before them upon the company’s closure.

Preference share capital can be redeemable or non-redeemable.

Redeemable preference share has a maturity date on which the company will repay the capital amount to the preference shareholders and discontinue the dividend payment thereon, while non-redeemable preference share which is also known as perpetual preference share, does not have a maturity date.

To calculate,

Total number of preference shares issued × Price per share

To calculate Preference Share Dividend,

Preference share capital × Rate of dividend

Dividend paid to redeemable preference shareholders are recorded in the Income Statement as an expense, while that paid to non-redeemable preference shareholders are deducted against the retained earnings.

Debentures

Debentures are long-term loans to the company with a fixed rate of interest payable regardless of the business’ profit performance. Therefore, debentures are recorded as a Non-Current Liability in the Statement of financial position.

Since debenture holders are not considered members of the company, they do not have voting rights at the shareholders’ meetings.

Interest on debentures are recorded as an Expense in the Income Statement and are paid before shareholders dividend.

Upon the company’s closure, debenture holders are paid before any capital shareholders.

General Reserves & Retained Earnings

General Reserves are profit for the year that was kept aside to meet the company’s future development.

To calculate,

Beginning balance + Transfer during the year

Retained Earnings is an accumulation of profit after distribution of dividends and transfer to general reserves from the beginning of the company’s operation.

To calculate,

Beginning balance + Profit for the year – Transfer to general reserves – Ordinary share dividend paid

Statement of Changes in Equity

This statement is prepared to explain how profit for the year was divided and comprises of four columns namely, ordinary share, general reserves, retained earnings and a total column.

It starts with the balance at the beginning of accounting year. This is amount brought forward from the previous accounting year.

Next, profit for the year after deducting dividend paid and owing to redeemable preference shareholders, is added to retained earnings.

Any transfer to the general reserves is added to the general reserve and deducted from retained earnings.

The interim dividend paid in the current year is deducted from retained earnings, while the proposed dividend is not, as it has not yet been paid.

The payment of the previous year’s final dividend is deducted from retained earnings.

Finally, each column is totaled, and the balances are carried forward to the next accounting year.

Recording in the Financial Statements

Income Statement

The income statement of a limited company is prepared on the same basis as that of a sole proprietor. However, there are two expenses that are unique to a limited company. They are Interest on debentures and Dividend to Redeemable Preference Shares.

Statement of financial position

The shareholder’s equity portion of a limited company comprises of non-redeemable preference shares, ordinary shares, general reserves and retained earnings.

In the non-current liability portion, it may contain debentures and redeemable preference shares.

And in the current liability portion, it may contain unpaid interest on debentures and unpaid dividend for redeemable preference shares.